Problems persist despite the reform…

The reform the EU Securitisation is not the expected game changer for the European asset-backed markets

The first conclusion of this survey, carried out by the AFME with the actors of the European asset-backed markets is that the reform put in place for nearly 3 years has not fulfilled its functions.

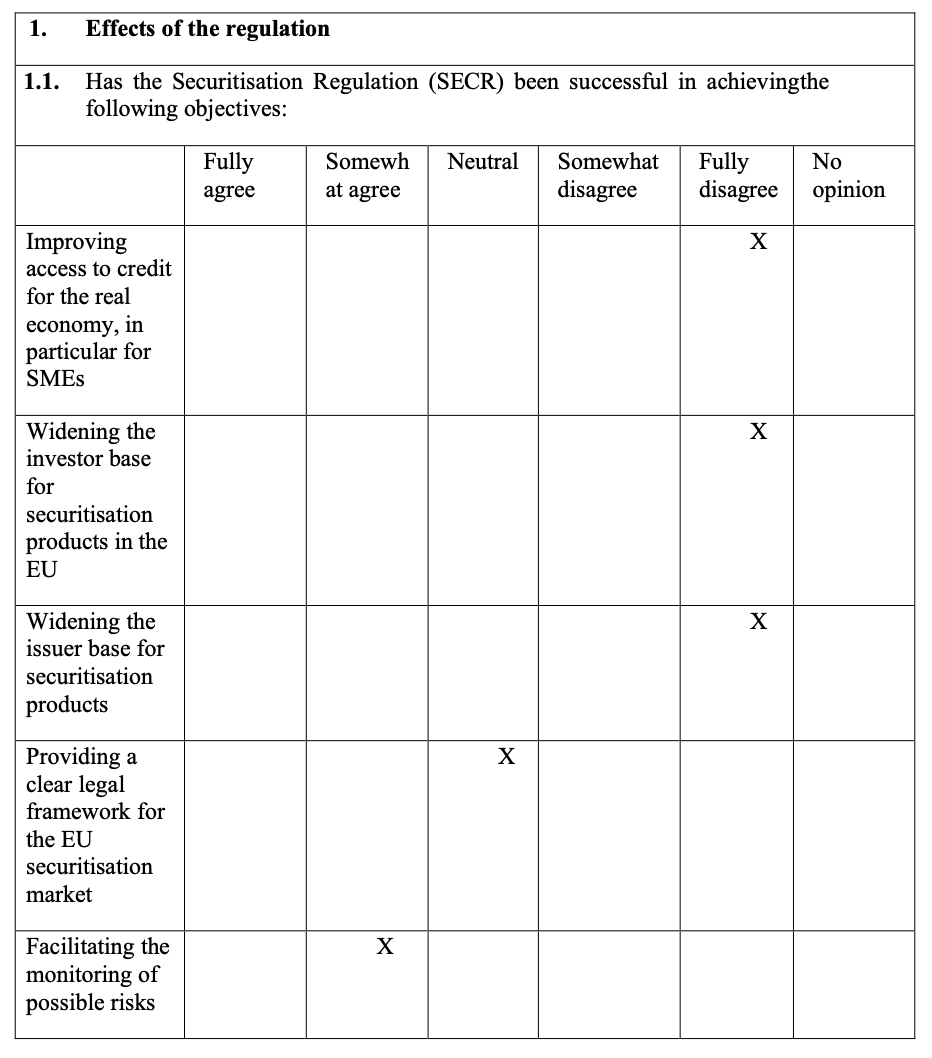

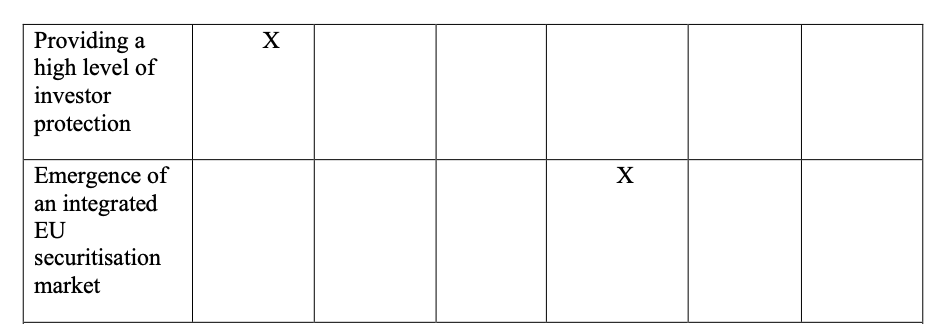

Below is the summary table of the market players’ opinions about the effects of the reform, published at the beginning of the survey, that explicitly shows their disappointment.

General result table from the survey about the Securitization Regulation

The results of the feelings of the actors interviewed by AFME are clear and unambiguous in terms of the primary objectives of this reform:

They are very disappointed with the effects on the reform when it comes to increasing liquidity on these asset-backed products. There are just a few more or sometimes even less asset-backed issuers and investors than before the reform.

The feeling about the emergence of a clear and standardized legal framework in Europe, regarding the documentation of asset-backed instruments is neutral.

Yes, this reform has clarified a lot of points, but it has taken longer than expected to be put in place, with some grey areas still present.

These gaps make us say that yes, it is better than before and that it creates a unity for the European asset-backed market, but in order to have a real solid European asset-backed framework, there are still ways to go.

Furthermore, although it is not the only factor, it will only help to broaden this market to the new players decried in the previous point

The only impact of this EU reform is on the protection it gives to investors. According to the various players in this market, investors are even more protected than before whenever they invest in these products.

So why is the trend, despite this reform, downward and the report so negative about the attractiveness of this market?

Onbrane’s understanding of European asset-backed market issues

At Onbrane, we met with the major asset-backed market players in France and Europe at the very beginning of the project. Indeed, they are key players in the commercial paper market, particularly in the US, and due to the volume of issuances they represent. Very quickly the recurring problems of these products in Europe were raised:

1- a lack of digitalization, which makes the legal constraints (sending new versioning of the various contracts…) to the already existing counterparties cumbersome

2- a crying lack of liquidity in Europe. For the NEU CP (French CP market) an infime part of the global outstanding is issued by asset-backed issuers ( around €5B for a total outstanding of €250B) where in the USCP market, asset-backed outstandings are way more significant ($275B for a total outstanding of $1,1B in September 2021).

The asset-backed commercial papers are ignored by most of the European investors. Besides, we have learned from asset-backed issuers that for them this is all the more damaging as they do not know where it is stuck. Indeed, feedback they get from investors’ credit analysts is often very good.

The product is quite well-known from every actor in the market but may still have a bad reputation from the subprime crises and the euro crisis of 2012. Investors are also afraid of securitization because they see these products as very complex and obscure.

…but good solutions have been set up and need to be taken further…

The possible improvements asked by the survey for better European asset-backed markets.

Despite the negative findings, this reform was a step in the right direction.

Standardization remains a very good initiative following the various economic crises to restore the confidence of players in asset-backed markets.

The SECR and simple transparent and standardised securitisation (“STS” and “STS Securitisation”) should be clarified and simplified in many subjects, in order to improve transparency and efficiency in the sharing of legal and marketing information. It is up to the authorities to take the reform further.

The treatment of STS securitisations and asset-backed commercial papers(ABCPs) for the liquidity coverage ratio (LCR) could be upgraded in order to improve the liquidity on these products.

The asset-backed products must be attractive, and things have already been done in that direction. For example, the standardisation of asset-backed green or sustainable products can meet the growing needs of investors for these investments.

However, once again, the framework is too restricted today to very few asset classes and this needs to be remedied by the authorities.

Finally, digitalization will be key for this market. The current counterparties in place must have a large number of interactions on the exchange of legal documents which are often updated. They also need to share, explain and give interest to new stakeholders.

These two main tasks are often done manually and are time consuming. Moreover, digitalization will help monitor asset-backed trades throughout the life of the financial instrument issued, as well as the underlying assets and the vehicle that was financed.

The monitoring will be simpler, transparent and instantaneous which will also help gain confidence in these markets for better liquidity.

The specific module built on Onbrane to share the asset-backed Framework

With Onbrane, we want to participate in the creation of a true European asset-backed market. Obviously we cannot act on all the problems, especially legal ones, but we want to accelerate the digitalization and integration of asset-backed frameworks into the European commercial paper market (to start with, then other financial instruments!)

At Onbrane, we built a unique tool that will allow the asset-backed pre-negotiation to be very efficient

Our debt issuance and trading platform, which brings together all types of market players, has always fully integrated asset-backed players who can trade their product like any of the other players, but also have access to a specific pre-trade module to share their asset-backed framework through it.

The Onbrane asset-backed module is:

A stand-alone module that can be used with any debt product to negotiate and issue asset-backed trades on Onbrane.

A collaborative tool between issuers, intermediaries, investors, credit risk analysts etc. in order to present, interact with and share all documentation regarding the underlying assets and agreements with the securitization (liquidity contract with the sponsor bank,…)

A modern, standardized and dynamic PDF-Killer tool to present, share and validate the framework, projects, KPIs, reports, and so on.

More precisely, we have created a module that standardizes the presentation of the asset-backed framework while giving issuers total freedom as to what information they share on their frameworks and to whom they share it with (internally for their teams, their established counterparties, new investors present on Onbrane).

Each time a debt security is issued, the asset-backed issuer may link it to its Framework or to one or more of its SPEs that have been refinanced by this transaction.

The monitoring of the trade and the underlying is thus ensured throughout the life of the debt and even beyond.

Everything from the pre-trade to the end of the debt is concentrated on a simple, transparent, collaborative and efficient platform. What a way to reconcile the European market to these products!

PS: a similar module has been created to share the green and sustainable frameworks, which are also reliable for debt issuance: issuing green asset-backed debt on Onbrane is possible!

…for allowing the emergence of a fully transparent, dynamic and integrated European asset-backed markets

Much has been done to enhance the value of asset-backed products, whether through standardization or by opening these products to green and sustainable labels.

The report therefore severely judged the real effects of the reform on the standardization of asset-backed markets. Its implementation has not yet produced sufficiently visible results and the negative trend in Europe remains light years ahead of the US asset-backed market.

The number of players is not increasing, much like the liquidity, the accessibility to these financial instruments remains complicated and its attractiveness – low.

For the sustainable part, there is also a lack of clarity which reduces the possibility to issue sustainable asset-backed products to certain asset categories.

However, tracks are given to change the situation: efforts are requested, for the authorities to push even further for the simplification of the asset-backed frameworks and with that, reduce the legal burden.

The authorities are also expected to give official recognition to these instruments by giving them better ratings, which they deserve in view of their characteristics.

One big demand is to qualify STS ABCP as Level 2A assets instead of Level 2B.

On the other hand, technological solutions, such as the one created by Onbrane, seek to energize this market by connecting established market players with new counterparties and fostering exchanges and collaboration to make this product more accessible and transparent.

Digitalization can definitely help the growth of this important market in Europe. By letting all the actors communicate while also letting them collaborate and monitor the trades, Onbrane wants to play a key role in the emergence of a real European asset-backed market!

Read the entirety of the AFME survey → https://www.afme.eu/Portals/0/DispatchFeaturedImages/COM%20AFME%20Response%20to%20Article%2046%20Consultation%2030%20Sept%202021%20Submission.pdf